This is what would stop a Fed rate increase in March

With high inflation already a given, the Fed will be focused on the labour market and global considerations between now and lift-off in two months.

Washington | Global equity markets have been beside themselves trying to predict the Federal Reserve’s first move in its much-telegraphed plan to tighten monetary policy after years of zero or near-zero interest rates.

The big question now is whether, on the eve of its Open Market Committee meeting this week, the Fed will start the cycle in March with a 50 basis point increase to take its main policy target rate from zero-to-0.25 per cent to 0.50-0.75 per cent.

Federal Reserve chairman Jerome Powell. AP

Investors and pundits have built up a head of steam over the Fed’s expected post-meeting announcement on Wednesday (Thursday AEDT), not least because of the amount of money being bet on the outcome of both this meeting and the next.

The volume of put options – a contract giving the buyer the right to sell a stock at a locked-in price in the future (after the Fed’s announcements) – has reached its highest level since March last year, according to Bloomberg data.

Buying options allows the owner to cut their equity risk if they get their Fed prediction wrong.

Market participants are trading on the possibility that the Fed might not go as hard as people think.

But only two things will stop the Fed from bringing out the big wrench to tighten up loose monetary settings.

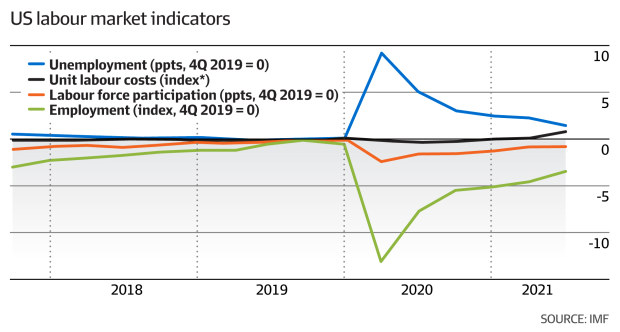

The US unemployment rate is 3.9 per cent, already below the long-term natural full-employment rate of 4 per cent, at which wages usually rise and stoke inflation. Bloomberg

Deutsche Bank’s chief US economist Matthew Luzzetti told The Australian Financial Review that the Fed would be looking at unemployment and financial market dysfunction between now and March.

The test for inflation – at a generational high of 7 per cent – is already too far gone.

“First, it would be back-to-back, what I would call ‘disastrous’ jobs reports between now and March, with the unemployment rate rising,” he said.

The US unemployment rate is 3.9 per cent, already below the long-term natural full-employment rate of 4 per cent, at which wages usually rise and stoke inflation.

There is some nervousness the omicron variant, with its related mandates for workers and school closures, has stalled the stunning jobs recovery, and may even have undone some of the gains.

But as Luzzetti points out, labour department reports would have to be “disastrous” for the Fed to react to this factor.

Fed chairman Jerome Powell has already indicated that with such high inflation, the central bank does not even need a full employment scenario to lift interest rates off their historic low level

“The second factor is getting really sharp, volatile and disruptive tightening of financial conditions in close proximity to that March meeting,” Luzzetti says.

Some suggest that tensions over Ukraine and related sanctions on Russia could trigger a financial crisis to which central banks – already low on dry powder – would have to respond with a more dovish approach to interest rates.

Euan Rellie, managing director for investment bank BDA Partners, says central banks have been known to get the jitters on geopolitical risks.

“I think people recognise interest rates have to go up. People recognise inflation is more persistent; it’s not transitory,” he says. “But conversely, or perversely, the Fed typically turns a bit dovish when there’s real geopolitical risk in the market.”

Rellie says “conversely” and “perversely” because geopolitical risk in the case of Ukraine and Russia is likely to further stoke inflation – just the thing motivating the Fed to raise interest rates in the first place.

Ukraine is the third-largest grain exporter in the world, and Russia is responsible for 35 per cent of Europe’s natural gas. A war would further disrupt supply chains and feed through to energy and food inflation.

Financial market functionality is also important for the Fed.

“So it may be interesting to watch whether the Fed comes up a little softer on Wednesday than we expected,” Rellie says. “[The Fed] might even delay some of those interest rate [rises], or signal that they are potentially going to delay some of those interest rate rises.”

Bank of America analysts, however, say the Fed should not be relied upon to support financial markets.

“Investors should not assume the Fed will step in to placate volatile markets: inflation is at multi-decade highs, and the unemployment rate is sub-4 per cent.

“Given the central bank’s dual mandate, tightening is wholly appropriate,” Bank of America’s equity and quant strategist Savita Subramanian said in a note to clients.

On Tuesday (Wednesday AEDT), the much-watched 10–year Treasury yields rose 3 basis points in the last three hours of trading, reflecting market expectations that the Fed is not planning to go off-script.

Financial markets continue to price in four interest rate rises this year.

For Luzzetti, other than jobs and the financial market turmoil, “it seems close to a done deal that the Fed is going to begin to raise rates in March”.

Subscribe to gift this article

Gift 5 articles to anyone you choose each month when you subscribe.

Subscribe nowAlready a subscriber?

Introducing your Newsfeed

Follow the topics, people and companies that matter to you.

Find out moreRead More

Latest In North America

Fetching latest articles